No-Cost Retirement Income Planning Consultation

Are You Retired or Approaching Retirement

and Wondering How You'll Reach Your Income Goals?

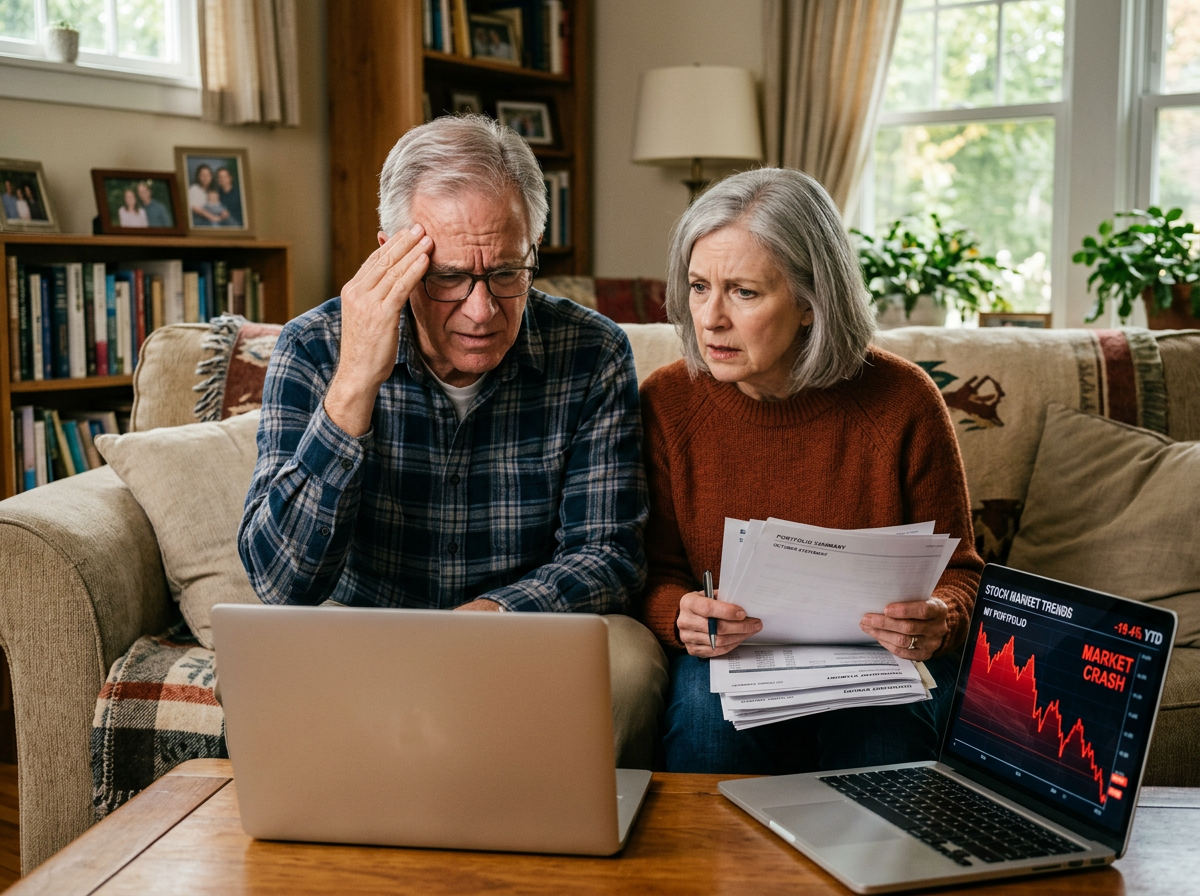

Perhaps you're concerned about stock market volatility or running out of money. Western Advisors is offering no-cost Retirement Income Planning Consultations to help you address these concerns.

- Compare your current plan's projected withdrawals to guaranteed income payments.

- Discover income that lasts for both you and your spouse — no matter how long you live.

- Consider allocating part of your assets to a vehicle that covers your basic living expenses and some discretionary expenses.